Banking has evolved significantly with the rising use of technology. With the digital transformation of financial services, the banking sector has become more accessible than ever.

People today use their smartphones to handle routine banking transactions and services, rather than standing in a queue at a branch.

Even in rural areas where brick-and-mortar banks may not reach, digital services have enabled the population to access banking services.

Key players in improving convenience and accessibility are Digital Banks & Neobanks. A lot of people, however, are often confused about these two terms.

The confusion is justified as both Digital Banks and Neobanks offer banking services digitally through a fintech app, and both are often used interchangeably.

However, is that correct?

Well, there is definitely a difference between a Neobank and a Digital Bank. And if you are wondering what they are, then this is the post for you.

In this one, we are going to compare Neobanks Vs. Digital banks and need to understand the key differences and similarities between the two.

So without further ado, let’s get started!

What Do the Stats Say About Digital Banks & Neobanks?

Banking has always been for the masses. And when something new appears in the global fintech market, it is the masses that decide its fate.

Fortunately, the market has certainly welcomed the idea of Neobanks and Digital Banks with open arms.

The reason behind this rising acceptance of digital banking is the penetration of smartphones and access to stable internet.

Not to mention, Neobanks reduce the hassles related to visiting a branch or filling out tedious formalities, making it more convenient for a user to rely on a digital account.

Here are key banking statistics highlighting this evolution:

- The global NeoBank market size was valued at approximately USD 230.55 billion in 2025 and is projected to reach USD 4396.58 billion by 2034, growing at a compound annual growth rate (CAGR) of 40.29%.

- NeoBanks typically offer fees that are 70% lower than those of traditional banks, making them an attractive option for cost-conscious consumers.

- 77% of NeoBank users report high satisfaction with their banking experience, compared to 56% for traditional banks.

- 70% of millennials prefer using mobile banking apps for their financial needs, emphasizing the importance of mobile-first banking solutions.

- Banks that have embraced digital transformation see a 20% increase in efficiency and a 15% reduction in operational costs.

- By the end of 2026, over 8 million Americans are expected to have accounts with a digital bank.

- 80% of NeoBanks use advanced security measures like biometric authentication and end-to-end encryption to protect user data.

- NeoBanks are projected to generate over USD 394 billion in revenue by 2026, driven by innovative financial products and services.

Going through the stats, you might have understood how digital banks and neobanks have changed the banking industry.

The shift towards digital banking is not just a trend but a fundamental change in how consumers and businesses manage their finances.

Before we draw a Neobank Vs Digital Bank comparison, it is important to learn about them both individually.

Hence, we will start with Neobanks in the next section!

What is a NeoBank? The New Era of Banking

Neobanks are digital banks that do not have a traditional banking system. Now what does that mean? Let’s simplify!

Generally, when we talk about banking, we visualize a building with a long queue and all manual operations.

Neobanks eliminate all the facade, making it purely digital and only about the necessary services.

These are banks that take a digital-first approach. Which means these have no physical branches, ATMs, or any brick-and-mortar stores related to them.

This completely digital solution allows a user to start their digital banking journey with all the basic features, including their savings and checking accounts, digital cards for online payments, simplified user experience, and more.

Let’s take a look at all the Neobank features below –

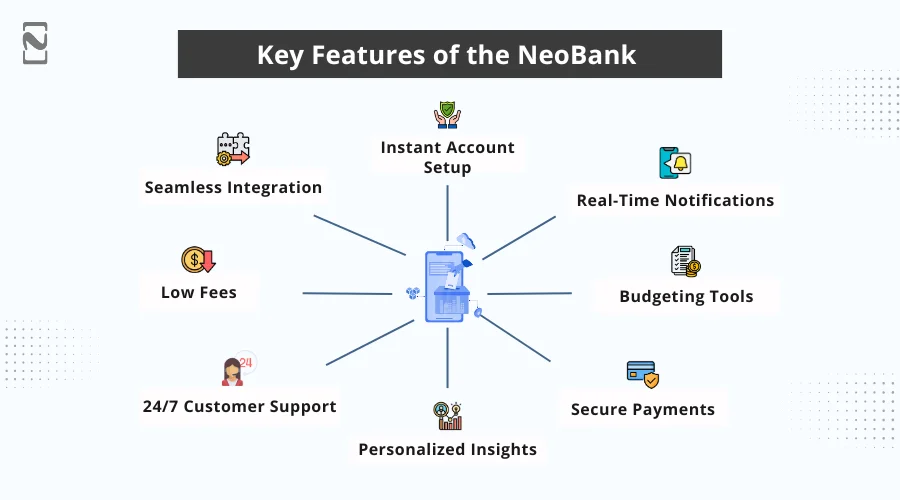

► NeoBank Features

Neobanks are a hit among users as they offer some of the best features a bank can offer.

Here’s a quick sneak peek into the features you can utilize when using a Neobank –

-

Instant Account Setup

Setting up your account with a Neobank is super easy, as all the steps can be done through your mobile app.

There’s no need to fill out a physical form or visit a branch; get your account from the convenience of your home.

-

Real-Time Notifications

Every transaction you make through a Neobank is updated in the system instantly.

Since the majority of Neobanks offer instant settlement of payments, it only makes sense to notify the user at the earliest.

-

Budgeting Tools

Neobank is more Gen-Z and Millennial-oriented. What do these generations want? The convenience of managing their finances.

Neobanks bring along additional features and tools for money management and budgeting for better retention on the application.

-

Secure Payments

When any transaction goes online, the prime concern of users is the security and privacy of the payments.

By implementing the latest encryption techniques, Neobanks ensure that the data is secure for every payment, from account transfers to peer-to-peer payments.

-

Personalized Insights

Neobanks are highly personalized and offer all the insights that a user may be interested in.

Since the services are 100% digital, insights can be retrieved as needed from anywhere in the world at any time.

-

24/7 Customer Support

One of the best benefits of a purely digital bank is that all its services are accessible 24/7, even customer support, which is a necessity in today’s age.

With the help of AI-enabled chatbots, queries can be registered and filtered instantly at any hour of the day, making it easier for the customer to share their issues.

-

Low Fees

Since neobanks are entirely online, the cost of infrastructure and maintaining resources is slightly lower than you would expect.

This is also the reason why these banks charge lower fees on transactions, making it more viable for new users.

-

Seamless Integration

Connecting a Neobank with other financial services and tools for a comprehensive financial management experience becomes easier for someone who uses a Neobank.

► Pros & Cons

Knowing all the features, let’s talk about the pros and cons that a Neobank brings along. You see, every coin has two sides.

Let’s start by exploring the brighter side and take a closer look at the pros of using a Neobank.

Pros:

- Convenience of accessing banking services anytime, anywhere.

- Significantly reduced fees and charges compared to traditional banks.

- Quick account setup and faster transaction processing.

- Highly personalized insights, tailored financial advice, and solutions.

- Advanced security measures to protect user data and transactions.

While Neobanks seem the best from the point of view of convenience, security, and personalization, they do lack in several areas that often are a deal breaker for many users.

What are these cons? Let’s take a look below!

Cons:

- Lack of in-person service might be a drawback for some users.

- Some NeoBanks may not offer the full range of services that traditional banks do.

- Internet connectivity is required for using Neobanks, which is not always available to everyone.

- Emerging regulations often impact the operations and service offerings of Neobanks.

► Example of NeoBank

Over the years, several Neobanks have emerged and have changed people’s perception of how Neobanks work.

Some of the prime examples of successful Neobanks are –

- Revolut

- Chime

- N26

- Monzo

- Starling Bank

The above information might have given you enough understanding of what a Neobank is and how it functions.

Now, in the next section, let’s break down digital banks so that we are ready for the Neobank Vs Digital Banks comparison.

What is Digital Banking? Modernization of Traditional Banks

Digital banking represents the evolution of traditional banking into the digital age. It involves the digitization of all banking activities for a traditional bank.

Digital banks offer these services through various online platforms, including mobile apps and websites.

Unlike neoBanks, which are entirely digital entities, digital banks are typically extensions of existing traditional banks that have embraced technology to enhance their service offerings.

The shift towards digital banking is driven by consumer demand for convenience, efficiency, and accessibility.

Customers can perform a wide range of banking activities, such as opening accounts, transferring money, paying bills, and applying for loans, without the need to visit a branch.

This digital transformation is supported by advanced technologies like artificial intelligence, machine learning, and blockchain.

This improves the speed, security, and personalization of banking services.

Digital banking also focuses on improving the customer experience by providing real-time notifications, personalized financial insights, and 24/7 customer support.

By adopting digital banking, traditional banks can reduce operational costs, reach a broader audience, and stay competitive in the rapidly changing financial landscape.

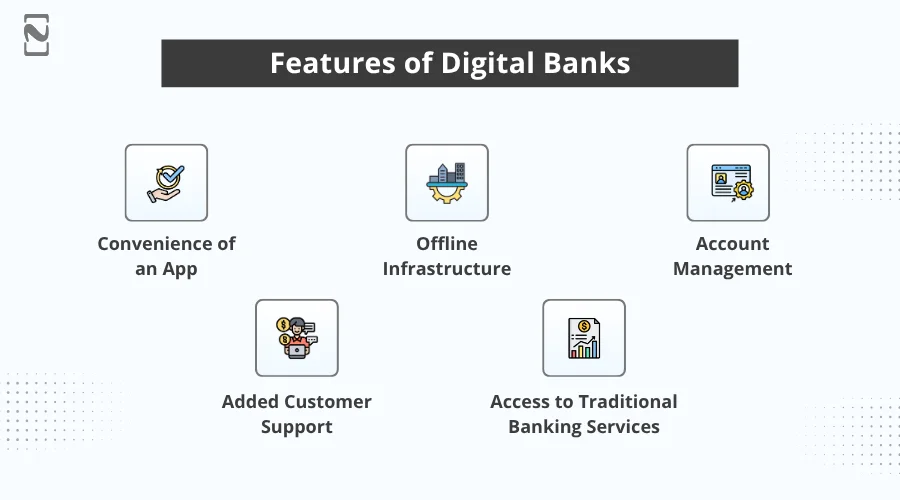

► Digital Banking Features

Digital banks are more like neobanks, but with the added advantage of offline support and a long-established customer relationship.

You see, the traditional banking system works on trust and physical banking services like branches, ATMs, etc.

When a traditional bank moves towards a digital solution, it combines the features of a brick-and-mortar bank and an online banking solution, bringing it all together for the users.

Hence, you may find some of the features coinciding with those of Neobanks.

Here are the features –

-

Convenience of an App

A Digital banking app for ease of access and convenience. People are always looking for ways to minimize the hassle when dealing with banking, and a convenient digital outlet does just that.

-

Offline Infrastructure

Availability of offline ATMs and banks (not applicable for all digital banks, but for those that have transitioned from traditional banking).

This makes it even easier for a user to access banking services in their vicinity, in case the internet is not available.

-

Account Management

Digital banks are well-equipped to handle all your account management needs, from upgrading your account type to downloading monthly statements.

Digital banking makes it simple with a banking app that does it all in a matter of minutes.

-

Added Customer Support

While offline banks already have their team of customer support experts, digital banks offer an added 24/7 service that makes it easier for the customer to actively address their issues whenever they want.

-

Access to Traditional Banking Services

While Neobanks only offer digital services and instant payments, Digital banks that are backed by a traditional bank can offer solutions like ordering a physical debit card, blocking the card, ordering a cheque book, etc., directly from the app.

Other than these highlighted features, digital banks can offer all the features that a Neobank has.

► Pros & Cons

The features of digital banks seem to have an upper edge over Neobanks, considering they bring along added offline availability.

However, it surely has its own downsides too. Let’s break down the pros and cons of digital banking to identify the same.

Pros:

- Allows access to banking services anytime, anywhere.

- Boosts transaction speed and reduces paperwork.

- The operational costs for banks can be minimized by saving on resources.

- Banks can collect crucial data to give out financial advice and services based on user data.

- Robust security measures protect user data and transactions.

The pros of using digital banking are already quite clear, especially for traditional banks that want to start their digital journey.

However, with added benefits, there are always some cons that slide under the radar. What are those cons? Take a look below!

Cons:

- Increased risk of cyberattacks and data breaches, especially for banks that are moving data from offline to a digital platform.

- Lack of in-person customer service might be a drawback for some users.

- Potential for the app or website downtimes that can disrupt services.

- Adapting to evolving regulations and ensuring compliance can be complex.

► Example of Digital Bank

Some of the prime examples of digital banks that are not Neobanks and have successfully made the transition are –

- Ally Bank U.S.

- Capital One 360

- Chase Online (JPMorgan Chase)

- Wells Fargo Online

- Barclays Online

With all that information, one thing that can be said with certainty is that the difference between Neobanks and Digital Banks is that –

All Neobanks are digital banks, but not all digital banks are Neobanks.

Now that we have established the necessary information about the two, let’s jump straight into the comparison and end this Neobank vs Digital Bank debate for once and for all!

What are the Differences Between NeoBanks & Digital Banks?

With both types of banking solutions unfolding in front of you in the previous sections, you might have already got an idea of the differences and similarities between Neobanks and Digital Banks.

To give you more clarity on the same, we have put together a table that puts Neobanks Vs Digital banks to draw a comparison.

Check out the table below –

| Features | NeoBank | Digital Bank |

| 1. Foundation | Digital-only from inception | Traditional banks transitioning to digital platforms |

| 2. Physical Branches | No physical branches | May have physical branches |

| 3. Account Setup | Quick and entirely online | Online with potential branch visits |

| 4. Fees | Lower fees, often fee-free | Higher fees compared to NeoBanks |

| 5. User Experience | Highly intuitive, tech-driven interface | Traditional interfaces with added digital features |

| 6. Security | Advanced security features like biometric authentication | Strong security, but it may vary depending on the bank’s tech adoption |

| 7. Customer Support | Digital-first support (chatbots, live chat) | A mix of digital and in-person support |

| 8. Services Offered | Focused on core banking modernization, some offer advanced features like crypto | Broad range of traditional banking services |

| 9. Innovation | Highly innovative and rapidly adopting new technologies | Steady innovators may lag behind NeoBanks |

| 10. Target Audience | Tech-savvy individuals and small businesses | Existing customers of traditional banks |

| 11. Examples | Revolut, Chime, N26, Monzo, Starling Bank | Ally Bank, Capital One 360, Chase Online, Wells Fargo Online, Barclays Online |

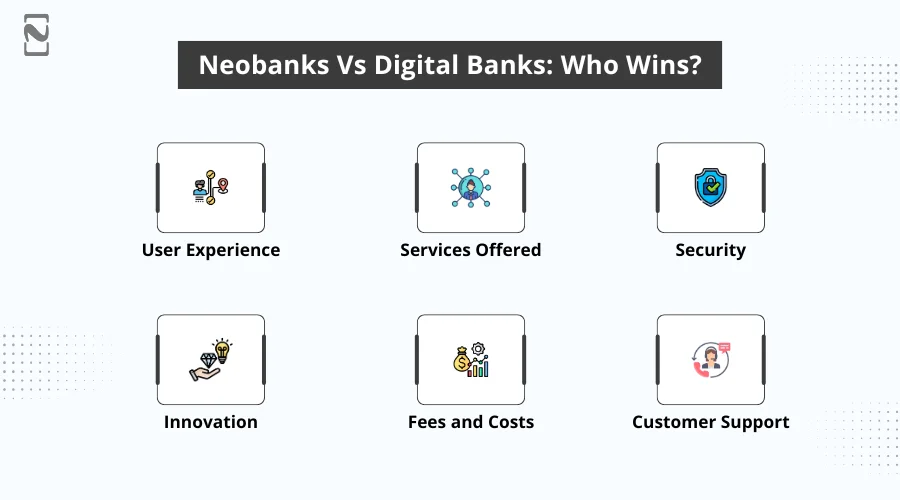

Neobanks Vs Digital Banks: Who Wins?

After comparing them both, it is certain that they have their differences and can be distinguished easily based on their foundation and several other factors.

Now let’s compare them based on different user-oriented factors to identify which one emerges out to be the best for an individual. Shall we?

1. User Experience

NeoBanks offers a highly intuitive, tech-driven user experience, focusing on seamless navigation, real-time notifications, and personalized financial insights.

Its interfaces are designed to cater to tech-savvy users who prefer managing their finances through mobile apps.

Digital Banks, while also providing digital platforms, often have interfaces that reflect their traditional banking roots.

They may not be as streamlined or innovative as NeoBank interfaces, but they still offer a wide range of services and a familiar layout for existing customers of traditional banks.

2. Services Offered

One of the major areas to compare in digital banking vs neobanks is the service offered.

NeoBanks typically focus on essential banking services such as savings and checking accounts, quick money transfers, and basic lending.

Some also venture into cryptocurrency trading and personalized financial advice. Their innovation lies in integrating advanced tech features to enhance these services.

Digital Banks, on the other hand, offer a broader range of traditional banking services, including comprehensive loan options, investment products, and insurance.

They leverage their established infrastructure to provide a full suite of banking services, which may appeal to a wider audience.

3. Security

Security is paramount in the age of information.

NeoBanks and Digital Banks prioritize security, but NeoBanks often employ cutting-edge technologies like biometric authentication and real-time fraud monitoring to protect user data.

Their digital-first approach allows for quicker adoption of the latest security measures.

Digital banks also maintain high-security standards, but their pace of adopting new technologies can be slower due to legacy systems and broader operational scopes.

However, their long-standing presence in the market often means they have robust, tested security protocols in place.

4. Innovation

Both NeoBanks and traditional banks, via digital banking, are driving innovation.

NeoBanks are known for their rapid innovation, continuously integrating new technologies and features to enhance the user experience and meet evolving customer needs.

This agility allows them to stay ahead in the competitive fintech landscape.

Digital banks innovate at a steadier pace, focusing on integrating new technologies into their existing frameworks.

While they may not be as quick to adopt new trends, their innovations are usually aimed at enhancing their comprehensive service offerings, providing a balanced blend of traditional and modern banking services.

5. Fees and Costs

Fee and cost are a big part when speaking of NeoBanks and digital banks.

NeoBanks generally have lower fees or even offer fee-free banking, making them attractive to cost-conscious consumers.

Their digital-only model reduces overhead costs, allowing them to pass on the savings to customers.

Digital banks, while often reducing fees for online services, may still have higher costs associated with maintaining physical branches and a broader range of services.

This can result in higher fees compared to NeoBanks, but they offer more extensive support and service options.

6. Customer Support

Lastly, let’s talk about customer support.

NeoBanks provides digital-first customer support through chatbots, live chats, and comprehensive online help centers.

This approach ensures quick and efficient resolution of customer issues, catering to the needs of digital-savvy users.

Digital Banks offer a mix of digital and in-person support, allowing customers to choose their preferred method of assistance.

While this hybrid approach can be beneficial for customers who prefer face-to-face interaction, it may not be as quick or efficient as the purely digital support offered by NeoBanks.

Neobank vs Digital Bank: Which Path to Choose as a Business?

Both NeoBanks and Digital Banks offer unique pathways into the fintech market.

If you are someone who is looking to understand the differences between the two to identify which path to choose for your fintech app development, then you can do the same by evaluating your business model, target audience, cost considerations, and desired level of innovation.

These factors can help you make an informed decision that aligns with your strategic goals in the fintech industry.

To sum it all up, you should go for

- Neobank if –

You are an entrepreneur with limited resources, aiming for quick market entry and focusing on tech-savvy customers.

Neobanks are also highly viable for businesses that prioritize rapid innovation and cost-efficiency.

- Digital Bank if –

You are an established financial institution looking to modernize and expand your digital presence.

Transitioning to a Digital Bank would leverage your existing customer base and infrastructure while embracing the benefits of digital transformation.

In both cases, you will need a solid banking software development company that understands the evolving market of banking and can help you with a digital solution.

Nimble AppGenie is certainly among the best companies from which you can hire developers to achieve the best mobile banking app for your business.

Conclusion

Choosing between starting a NeoBank or a Digital Bank depends on various factors, including your fintech business model, target audience, and available resources.

NeoBank offers a fully digital, innovative, and cost-effective approach, appealing to tech-savvy users and small businesses.

On the other hand, Digital Banks provide a comprehensive range of services, leveraging the established trust and infrastructure of traditional banks.

By carefully considering these aspects, entrepreneurs can make an informed decision that aligns with their strategic goals and market needs.

On that note, we have reached the end of this post. Hope the information shared gives you clarity on Neobanks Vs Digital Banks.

That will be all for this blog. Thanks for reading, good luck!

FAQs

NeoBanks operate entirely online without physical branches, focusing on innovation and lower fees. Digital Banks are traditional banks that have digitized their services while maintaining physical branches.

NeoBanks are generally more cost-effective to start due to lower operational costs, as they do not require physical branches.

Examples include Revolut, Chime, N26, Monzo and Starling Bank.

Examples include Ally Bank, Capital One 360, Chase Online, Wells Fargo Online, and Barclays Online.

NeoBanks must navigate a complex regulatory landscape, including obtaining necessary licenses and complying with anti-money laundering (AML) and Know Your Customer (KYC) regulations.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.